Salaries Expense increases (debit) and Salaries Payableincreases (credit) for $12,500 ($2,500 per employee × fiveemployees). The following are the updated ledger balances afterposting the adjusting when are adjusting entries prepared entry. Let’s say a company has five salaried employees, each earning$2,500 per month. In our example, assume that they do not get paidfor this work until the first of the next month.

- To avoid this mistake, it is important to record transactions as soon as possible and ensure that they are accurate.

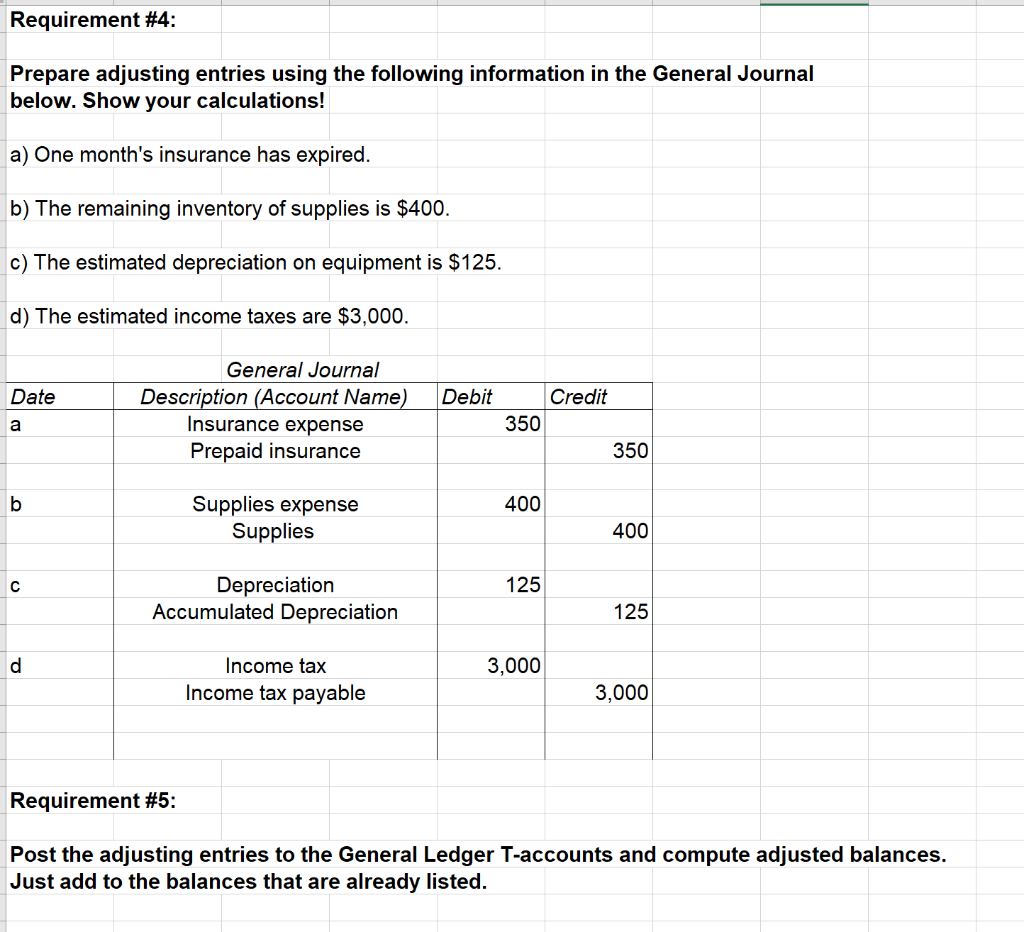

- Supplies Expense is an expense account, increasing (debit) for $150, and Supplies is an asset account, decreasing (credit) for $150.

- Income Tax Expense increases (debit) and Income Tax Payableincreases (credit) for $9,000.

- This transaction is recorded as a prepayment until the expenses are incurred.

- This concept is based on the time period principle which states that accounting records and activities can be divided into separate time periods.

2: Discuss the Adjustment Process and Illustrate Common Types of Adjusting Entries

For example, let’s say a company pays $2,000 for equipment that is supposed to last four years. The company wants to depreciate the asset over those four years equally. This means the asset will lose $500 in value each year ($2,000/four years). In the first year, the company would record the following adjusting entry to show depreciation of the equipment. If you create financial statements without taking adjusting entries into consideration, the financial health of your business will be completely distorted. Net income and the owner’s equity will be overstated, while expenses and liabilities understated.

Composition of an Adjusting Entry

For example, a company pays $4,500 for an insurance policy covering six months. It is the end of the first month and the company needs to record an adjusting entry to recognize the insurance used during the month. The following entries show the initial payment for the policy and the subsequent adjusting entry for one month of insurance usage.

Step 1: Print Out the Unadjusted Trial Balance

Recall that unearned revenue represents a customer’s advanced payment for a product or service that has yet to be provided by the company. Since the company has not yet provided the product or service, it cannot recognize the customer’s payment as revenue. At the end of a period, the company will review the account to see if any of the unearned revenue has been earned.

For example, if an adjustment entry is made to adjust the balance of a particular account that is related to a specific fiscal year, this will impact the financial statements for that fiscal year. This is a systematic way to prepare and post adjusting journal entries that accountants have been using for about 500 years. Interest expense arises from notes payable and other loan agreements. The company has accumulated interest during the period but has not recorded or paid the amount. This creates a liability that the company must pay at a future date.

Accounting Services

Before we look at recording and posting the mostcommon types of adjusting entries, we briefly discuss the varioustypes of adjusting entries. When a purchase return is partly returned by the customer, it is treated as a payment on account of the balance. It means that for this part, the supplier has received only a part of the amount due to him/her. In such cases, therefore an overdraft would be created in his books of accounts and he will have to adjust it when he receives the balance by making an adjusting entry.

So, your income and expenses won’t match up, and you won’t be able to accurately track revenue. Your financial statements will be inaccurate—which is bad news, since you need financial statements to make informed business decisions and accurately file taxes. Adjusting entries are changes to journal entries you’ve already recorded. Specifically, they make sure that the numbers you have recorded match up to the correct accounting periods.

The preparation of adjusting entries is the fifth step of the accounting cycle that starts after the preparation of the unadjusted trial balance. On September 30, 2022 (when the 12 months have expired), you would create another adjusting entry reflecting the rest of your prepaid rent (nine months or $15,000). Each entry adjust income and expenses to match the current period usage. The journal entry will divide income and expenses into the amounts that were used in the current period and defer the amounts that are going to be used in the current period. In the journal entry, Interest Receivable has a debit of $140.This is posted to the Interest Receivable T-account on the debitside (left side).

You’ll move January’s portion of the prepaid rent from an asset to an expense. Adjusting journal entries can also refer to financial reporting that corrects a mistake made earlier in the accounting period. Estimates are adjusting entries that record non-cash items, such as depreciation expense, allowance for doubtful accounts, or the inventory obsolescence reserve. In summary, adjusting journal entries are most commonly accruals, deferrals, and estimates. Adjusting journal entries can also refer to financial reporting that corrects a mistake made previously in the accounting period. An accrued expense basically means that you owe somebody something.